New Arrival Products

Hand Book for D.D.Os - A Hand Book for Drawing and Disbursing Officers

PKR: 1800

PKR: 1620

Encyclopedia of Electricity, NEPRA & WAPDA Laws

PKR: 5000

PKR: 4000

Principles of Tax Laws

PKR: 2500

PKR: 2250

![Central Public Works [Department Code, Account Code & Book of Forms]](https://www.petiwalabooks.com/images/thumbs/0006768_central-public-works-department-code-account-code-book-of-forms.jpeg "Central Public Works [Department Code, Account Code & Book of Forms]")

Central Public Works [Department Code, Account Code & Book of Forms]

PKR: 2500

PKR: 2250

A Hand Book for Office Procedure, Drafting & Noting

PKR: 500

PKR: 500

Practical Approach to Income Tax Litigation

PKR: 1200

PKR: 1080

Sindh Public Procurement Laws

PKR: 2500

PKR: 2250

Manual of Rent Laws

PKR: 3000

PKR: 2600

Sindh Local Government Manual

PKR: 4500

PKR: 3800

Hiba / Gift

PKR: 2000

PKR: 1600

Law of Pleadings in India and Pakistan

PKR: 5000

PKR: 3900

A Guide for the Sindh Drawing & Disbursing Officers

PKR: 4500

PKR: 4050

Sales Tax Act, 1990

PKR: 7500

PKR: 7000

Business Letters for Busy People

PKR: 750

Manual of Federal Civil Service Laws

PKR: 4500

PKR: 4050

Sindh Government Rules of Business 1986

PKR: 1800

PKR: 1620

The Income Tax Ordinance, 2001

PKR: 3200

PKR: 2900

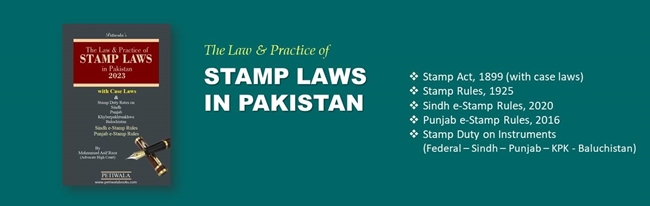

The Law & Practice of Stamp Laws

PKR: 3000

PKR: 2500

Understanding The Power of Ballots in Pakistan

PKR: 3500

PKR: 2700

Essential Business Letters

PKR: 750

Pakistan Army Laws

PKR: 2000

PKR: 1700

The Sindh Agricultural Income Tax Ordinance, 2000 & Rules, 2001

PKR: 600

PKR: 540

Compendium of Corporate Laws

PKR: 3500

PKR: 3000

اسلامی قانون وراثت

PKR: 500

PKR: 450

Drug Laws Manual

PKR: 5000

PKR: 4000

شہریوں کے حقوق و قوانین

PKR: 5000

PKR: 4000

Federal Tax Laws of Pakistan

PKR: 5000

PKR: 4500

Guide on Company Secretarial Practices 2023

PKR: 4500

PKR: 4000

Managing Corporate Laws and Compliances

PKR: 4500

PKR: 4000

Karachi Building and Town Planning Regulations, 2002 with Other Laws

PKR: 4500

PKR: 4000

Petiwala Stationary

Top Books

Women Harassment & Protection at Workplace with Rape Laws

PKR: 2000

PKR: 1600

Access to Justice in Pakistan

PKR: 4800

PKR: 3950

")

Services Problems & Solutions 2018 (Procedure & Practice)

PKR: 5000

PKR: 4000

4000 Questions for Cross Examination in Civil Cases

PKR: 3500

PKR: 2450

")

Audit Manual with Forms (With Forms)

PKR: 2000

PKR: 1800

Black’s Law Dictionary

PKR: 9000

PKR: 7500

Foreigner Laws

PKR: 1800

PKR: 1620

ذیابیطیس شوگر کا علاج اورانسداد

PKR: 500

پھلوں اور سبزیوں سے علاج

PKR: 400

PKR: 360

The Insurance Laws

PKR: 3200

PKR: 2880

Follow us